CEO Pay Insights from our 2017 UK CEO Value Index Research

While the United States begins the year grappling with their new CEO Pay Ratio disclosure and some significant tax law changes that impact CEO remuneration, the executive pay debate in the UK has reached a stage, politically, where it almost appears to be weaponised.

People have their points of view, of course, and ours is grounded in pay-for-performance facts. We have taken a look at the way executive pay stories emerged in the business press, and then considered how those same stories might have been covered if they were using a broader set of facts. For example, we focus on the value an executive delivers to shareholders, not just the cost of their pay package.

First, let’s take a quick look at how the press covered executive pay stories for five companies.

Imperial Brands: The Guardian in January 2017 reports on shareholders blocking a raise for the CEO “in a move that may affect other FTSE 100 companies aiming to hike the bonuses of their bosses.” The article further notes, “Critics of high pay said the move was a warning to company bosses about pushing through pay rises - but urged investors to keep up the pressure.”

Reckitt Benckiser: The Financial Times in March 2017 covers an “investor revolt” at the company where CEO Rakesh Kapoor “would have been entitled to an additional £14m last year—mostly from a long-term incentive plan—had the remuneration committee not decided ‘to exercise discretion’ in curbing his pay.” The piece notes that “Reckitt promised to listen and ‘take very seriously’ comments from shareholders.”

Shire and AstraZeneca: In April 2017, City A.M. discussed pharmaceutical giants Shire and AstraZeneca as facing “another shareholder spring as corporate governance consultants slam executive pay ahead of investor votes.” At Shire, the article reports experts have “multiple concerns over a complex system and overly generous rewards.”

Burberry: A July 2017 edition of The Guardian leads with “A third of Burberry’s shareholders have failed to back the luxury brand’s remuneration report in a protest over high pay. Investors representing just over 32% of voting shares rejected the report with more investors withholding their votes despite recent attempts to appease their anger by reducing overall pay deals.”

This is remarkably similar, somewhat negative coverage and to be fair many of these news sources are simply reporting a broadly covered story. But does a comparison of the above companies using the data from our UK CEO Value Index provide a rather different angle on these stories?

You can be the judge. The following charts show those same companies from three different perspectives.

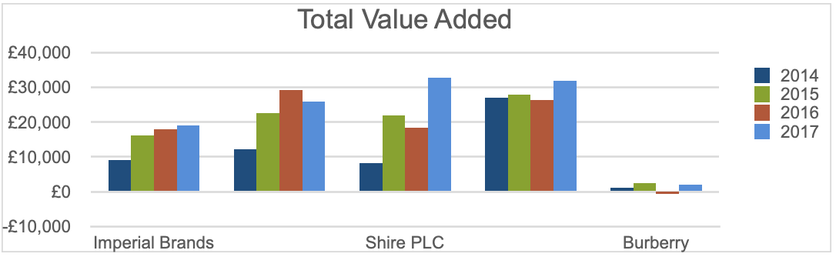

Total Value Added: This is the amount of money which all of the shareholders gained from increases in value, reinvested dividends, and share buybacks over a four-year period, ending in the years shown.

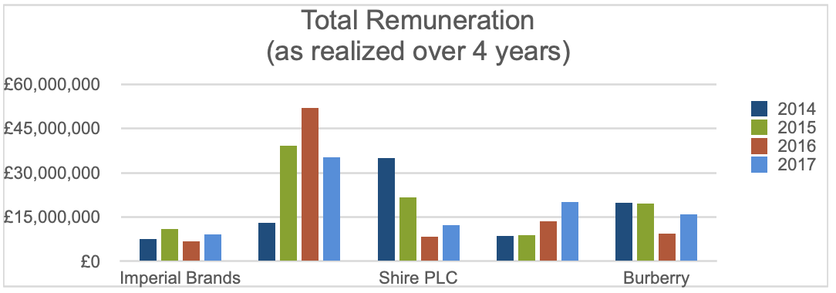

Total Remuneration: This is the total amount the CEO was paid in realised compensation over the same four-year periods, ending in the years shown, including salary, actual bonus, and vested long-term incentives.

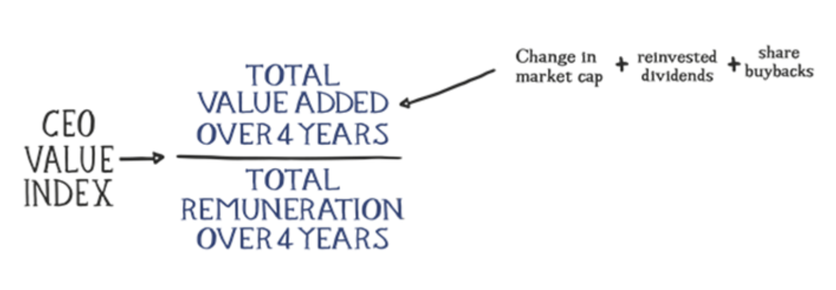

The UK CEO Value Index: Before we look at additional data, here is a quick review of how the Index works.

We offer a simple “rule-of-thumb” to guide compensation decision-making. It measures how much value a CEO adds to their company for every pound they are paid. We look at value added to shareholders over four years, which captures change in market cap, dividends, and share buybacks, and we divide that by the total realized pay for the CEO over the same period.

The findings offer shareholders, compensation committees, total reward professionals, regulators, and commentators the opportunity to calibrate and evaluate pay programmes in a number of important ways.

For shareholders there is clear and immediate evidence of whether leadership is delivering value, relative to the total pay opportunity being offered; and a simple comparison across sectors by company size and over time.

For boards and HR teams there is the ability to review the results of incentive compensation design; an opportunity to ask how well pay aligns with performance and how that pay to performance alignment compares with other relevant comparators; and the ability to calibrate future performance requirements, given “benchmark” pay.

For regulators and commentators there is a comprehensive view of pay and performance over time, across sectors and across geographies; and a snapshot of pay-to-performance alignment, providing an objective commentary on the impact (or lack of impact) of regulatory changes.

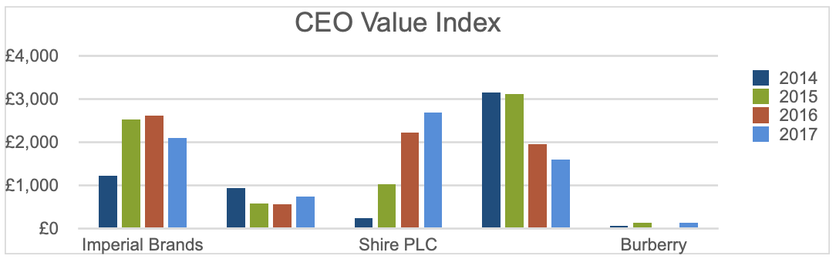

With that background, here is a look at how our five companies in question have performed.

Our Conclusions

The productivity of the CEO compensation programmes is markedly different (lower) at Burberry, yet the others share equal opprobrium—perhaps because the “headline” pay figures are broadly the same. Is that fair? It is if you are simply criticising anyone, whomever they may be, for whatever reason, for making lots of money. But, that’s not how the system should really work. If you are good, and you create value for all those shareholders, you deserve reward.

In comparative terms, if we select out Burberry as poor value for the money, given shareholders’ investment in executive pay, the other four companies have all done reasonably well or very well, in their own way.

Shire has improved a great deal—that is a high (and increasing) performance story combined with relatively modest (and decreasing) CEO pay opportunity.

Imperial Brands and AstraZeneca have a consistently high Value Index, although AstraZeneca’s productivity vis-a-vis pay and performance has fallen away slightly.

The Reckitt Benckiser story could have been handled differently. That company and its board could point to an impressively high total value added figure, although the CEO’s remuneration is highest of all. Our view is that their remuneration committee might re-calibrate the pay opportunity to deliver a higher Index outcome, but should not shy away from a high pay opportunity given the consistently high value created for stockholders.

Calibrating a programme that can deliver a “winning” Index ranking is not easy for remuneration committees. If we look at who the winners are in terms of the Index, there are a handful that tend to rank highly year over year; Imperial Brands and AstraZeneca are among them. This suggests that it is possible to arrive at a finely tuned pay programme that is aligned with company performance. And that is a headline we should be seeing.