Global Executive Remuneration Themes Reflections from the UK

The Rem.n London Team co-sponsored the City Remuneration Summit in London this year, and the meeting covered some very interesting ground. There was a good mix of speakers and expert panels, which I think works well as a structure for passing on complex material. The experience on hand amongst the various speakers and contributors included a broad array, from lawyers, consultants, directors of reward, and remuneration committee chairs to doctors, HR practitioners and retired HR leaders.

We covered subjects that ranged from the tactical (dealing with mental health issues, creating healthy corporate cultures, and understanding and managing the new financial services regulations and malus and clawback provisions), to the strategic (where remuneration is going over the next few years, globally).

My contribution was focused on the global picture, and in addition to discussing how incentive compensation—the basic principles of reward-for-performance—works and the world-wide commonality of this principle, we covered three emerging topic areas:

- The growth and importance of Environmental Social and Governance (‘ESG’) metrics;

- The push towards Economic Value Added (‘EVA’ or ‘Economic Profit’) from the US, where the proxy voting agency ISS is making important changes in its perspective on performance; and

- Gender and equality.

ESG Metrics

The various ‘non-financial’ ESG measures which cover environmental, social and governance aspects of business performance are increasingly a matter of great interest to investors and other stakeholders.

In the past, governance was closely viewed by the proxy agencies as board structure, compensation, shareholder rights and audit and risk assessment.

But now, and increasingly, the ‘E’ and ‘S’ factors are being addressed. In the case of environmental that is:

- Environmental actions (e.g., cutting plastic usage such as Unilever’s goal to reduce plastic packaging by 50%);

- Carbon emissions and the impact on climate change (e.g., goals from BP, Shell, etc., such as cutting greenhouse gas emissions);

- Sustainable natural resource use (e.g., reducing or eliminating clear-cutting of forest acres); and

- Reducing overall waste and toxicity.

And in the case of social: human rights, labour, health and safety (note: safety is typically one of the earliest ESG metrics adopted).

As controversial as this may sound, the impact of environmental measures in incentive compensation might prove to be more effective than active protests (which were coincidently ongoing in London, during our conference). That is because:

- Executives generally do what they are paid to do;

- Environmental goals can be set at a very granular level and are measurable and auditable;

- Many of the companies adopting or considering ESG goals are huge, and any change in their environmental sustainability policies can be massive; and

- There are emerging pressures from investors (like Blackrock and activist hedge funds) to ensure this gets greater and greater exposure.

I believe the same is true of social issues, as well.

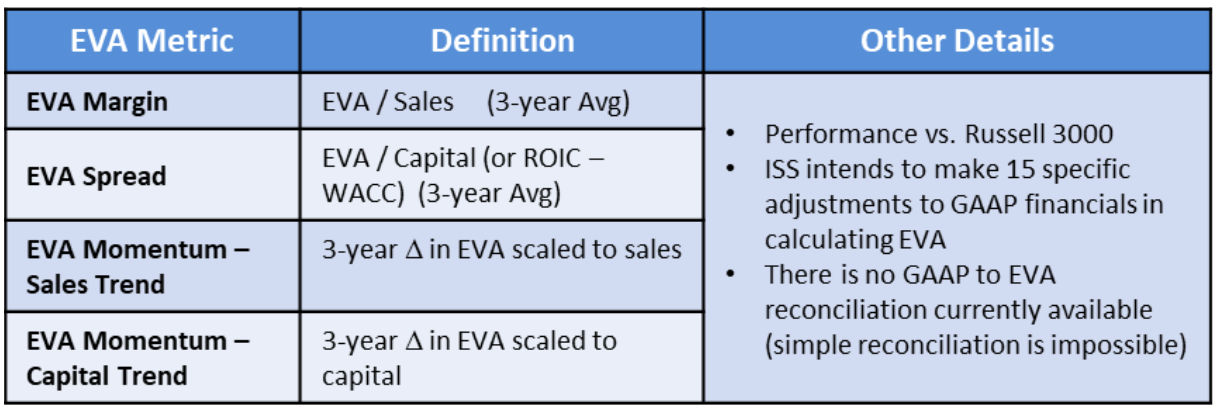

Economic Value Added (‘EVA’) or Economic Profit

This metric is already being used by some firms, around the world. What is interesting is that its use is now promoted by the US-based proxy advisor ISS. The ISS pay-for-performance (PFP) test will likely include EVA measures beginning in 2020.

The current ISS Performance Tests are:

- Test 1: Absolute and relative Total Shareholder Returns (‘TSR’)

- Test 2: Secondary test covering three to four financial metrics such as ROIC, ROA, ROE, EBITDA, operating cashflow, etc.

- In 2020 we’ll see weighted EVA metrics including:

In our experience we have helped clients install EVA as a metric, but we are cautious. Why?

- Complexity of the metric, particularly the assumptions and calculations required to adjust the capital charge;

- Companies’ lack of familiarity with the metric;

- Its long history of poor implementation within compensation plans;

- A worrying tendency for ‘true believers’ to see EVA as a panacea for all issues, not simply growth, profitability and capital efficiency; and

- For broad-based comparative purposes, EVA appears no better than other metric combinations.

This is the first occasion in my memory where the US remuneration governance recommendations have leap-frogged those in the UK. The UK has tended to be more onerous in most areas. Either way, it is coming in your direction!

Gender Pay Gap and Equity

We covered the important difference between the ‘pay gap’ (something we are used to in the UK legislation); pay equity, defined as equal pay for equal work and which is built into US Federal legislation; and pay equity, when it is more broadly defined as equal pay for comparable work and built in selective US state legislation.

Pay equity has not generally proven to be the large issue. As my US colleague Kathy Baron notes in her recent article, “The often-reported statistic that a woman earns 80 cents for every dollar that a man earns has not generally come about due to pay equity issues, but more due to representation in leadership positions, career sorting, career disruption, and unconscious bias.” The UK legislation on disclosure has added much to this conversation, but don’t look for it to either solve the issue or lower the volume of debate. Remuneration committees should be taking note—again, this is coming in your direction!