A Look Back at the FTSE 350 and Executive Compensation in 2020

As we approach the holidays, we take a moment to look back at how companies have weathered the onslaught brought on by a global pandemic. Specifically, we look at the FTSE 350—how have companies performed, how have companies responded with respect to executive compensation, and what might we see in 2021?

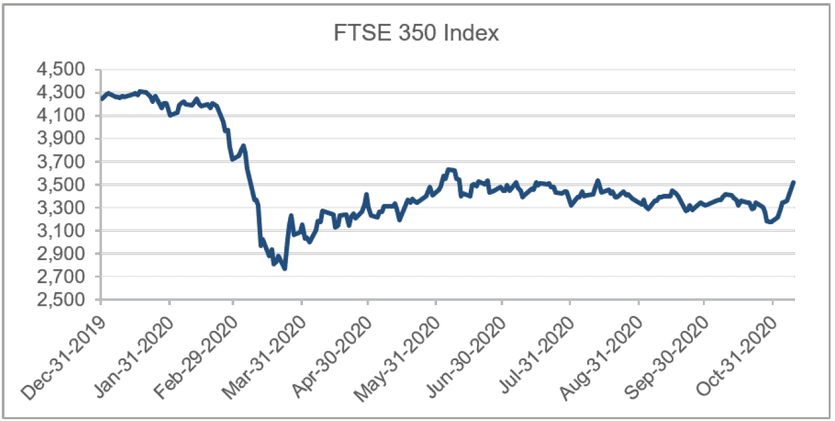

The graph below shows the performance of the FTSE 350 Index since the beginning of the year. The FTSE 100 and FTSE 250 have seen very similar patterns in their relative performances over the course of the year with the very biggest companies suffering alongside some of their considerably smaller counterparts.

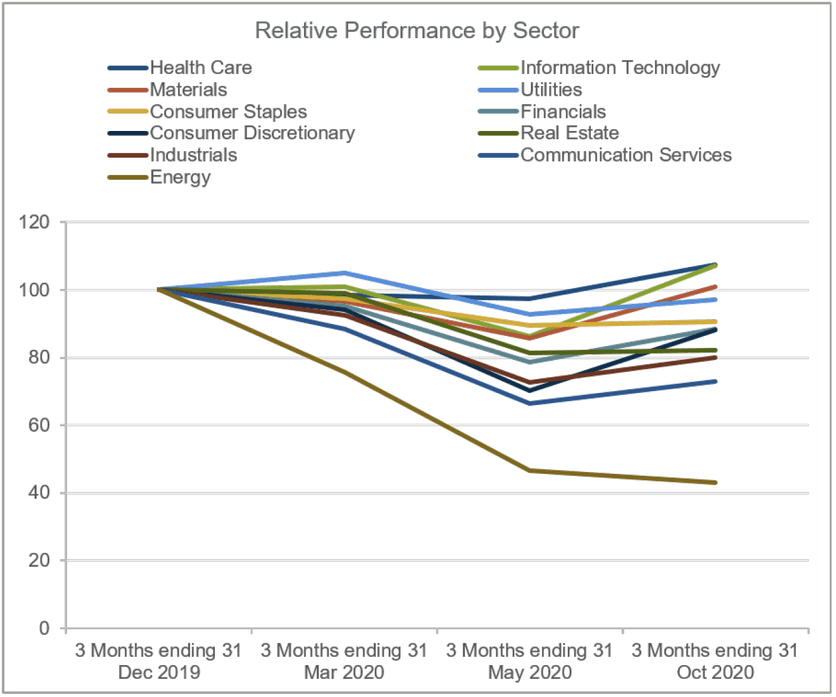

Whilst no business is immune, it is not surprising that some sectors have been more, or less, severely affected. The graph below looks at the relative changes in market cap by sector since the beginning of the year. It looks at the average market cap of each sector in the FTSE 350 at three different points in time over the course of the year versus the three months ending 31 December 2019.

Leading the way and rebounding strongly are companies that sit within the healthcare and information technology sectors whilst those in the energy sector continue to struggle amidst heavily depressed oil prices. For the energy sector, this dip is happening in the wider context of a decrease in fossil fuel demand driven by a growing commitment towards decarbonisation—an issue that will continue to play out long after this pandemic passes.

Looking at the graph above, all sectors, with the exception of the energy sector, experienced at least a small uptick in average performance (measured by market cap) for the three months ending 31 October 2020. This uptick coincides with a period of relative normality with the majority of businesses allowed to open (albeit with restrictions).

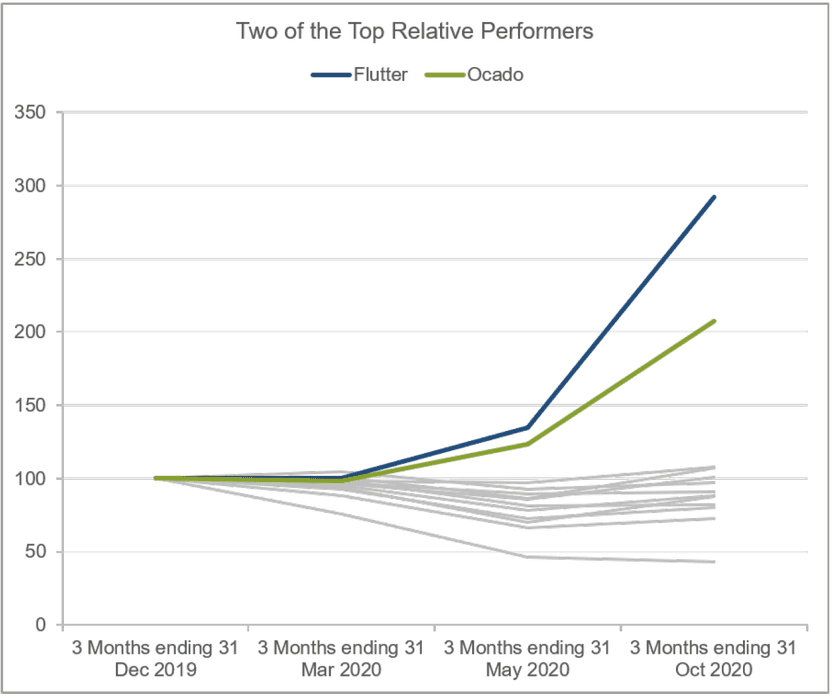

The graph below looks at two companies that despite remarkable relative performance may still face challenges from shareholders.

Flutter Entertainment has seen exceptional growth over the period bolstered by the completion of its acquisition of The Stars Group. Whilst Flutter may not have taken any government money under the furlough scheme and has committed to retaining all its employees (despite the closure of its high street stores), it did suspend its interim dividend to shareholders. In an undeniably challenging time, there is no doubt that Flutter has performed well, but the decision facing the remuneration committee is still not straightforward—particularly with respect to bonus outcomes. The year is not yet over so whether or not performance targets will be hit is still to be decided but a recent announcement from Legal & General suggested that bonuses should not be paid for the 2020 financial year in cases where dividends have been suspended.

Fellow top performer Ocado finds itself in even trickier waters with 30% of shareholders voting against Ocado’s remuneration report at this year’s annual general meeting (AGM), rising from 24% the previous year. Whilst Ocado may have seen exceptional growth not only during the pandemic but also during prior years, shareholders are concerned that pay levels are excessive. This is where the London Team's UK CEO Value Index becomes a useful tool allowing remuneration committees and shareholders to use an alternative lens to assess the cost of the CEO versus the value added. It essentially calculates value added (measured by market cap, reinvested dividends and share buybacks) per pound paid to the CEO over a four-year period. Initial calculations show that for the four-year period ending 31 December 2019 Ocado quadrupled its market capitalisation. Despite this, its UK CEO Value Index score for the period is 102 suggesting that shareholders are perhaps on the money with their assessment. For reference the very best value companies typically achieve Index scores well above 1,500.

Whilst Flutter and Ocado may not have reported any adjustments to their executive pay arrangements over the course of the year, many companies have had to. The optics of executives continuing to cash in their paycheques whilst the threat of unemployment and family and community hardship grows is simply not defensible. Overall executive salaries have been cut at more than a third of FTSE 350 companies for at least some period of time over the course of the year.

In those sectors hit most acutely responses were almost immediate whilst for the largest banks, changes were requested by the Prudential Regulation Authority (PRA). The proposal from the PRA agreed by the UK’s seven largest banks banned dividends, buybacks, and cash bonus payments to top management and material risk takers in a bid to conserve cash. Some banks have gone a step further, for instance Barclays Chairman, CEO, and FD donated a third of their fixed pay for six months to charities supporting vulnerable people affected by COVID-19. Nationwide went a step further again with the CEO and board volunteering a 20% cut in base salary and pension, and net fees respectively for 2020/21 in addition to reducing performance pay opportunities for next year to one third of their current level.

What’s the outlook for next year?

There is a deafening expectation that executives must share the pain and be aligned with their wider workforce. In a year where executive teams and boards have had to work harder than ever in entirely unprecedented circumstances that is understandably going to cause some headaches. Yet the message from shareholders is clear: if the business is suffering, if the workforce is suffering, if the shareholders are suffering, then executive pay must reflect this.

Shareholders are already issuing warnings for the 2021 AGM season:

- Legal & General announced they would not support any increases to annual bonuses. They also announced that they may vote against any company that took money from the government or shareholders (via additional capital or suspended dividend) if they pay a bonus for the 2020 financial year. On that basis alone we can expect to see a very large proportion of companies paying nil bonuses.

- The Investment Association (IA) has taken a similar view, albeit with a slightly more forgiving stance on indirect government support and suspended/cancelled dividends. In those cases, they are advising that remuneration committees must make it clear how these events have been taken into account and their respective impacts on remuneration outcomes through the use of discretion or malus provisions. The IA also warns against windfall gains from LTIP grants made in 2020 and the importance of continuing to set appropriate performance metrics. For many companies restricted share schemes are no doubt looking like an attractive option with no need to calibrate performance metrics. Yet the IA warns that a shift to a restricted share scheme must be made on the basis that it is strategically right as opposed to mitigating the challenges of defining performance targets.

Those companies with earlier year-ends are already feeling the effect of stricter shareholder voting. In November, more than 35% of Galliford Try shareholders voted against the remuneration report on account of the remuneration committee exercising its right to use discretion to change the bonus criteria during the year. ISS advised shareholders that this adjustment resulted in bonus outcomes that simply weren’t commensurate with the company’s overall performance or the shareholder experience.

Whilst next year’s AGM season will be one of a kind, the remuneration committee will continue to feel the impact of this pandemic for many AGMs to come. In 2023 remuneration committees will be sitting down to determine if LTIP grants made in 2020, when share prices were at an all-time low, have resulted in windfall gains for executive directors. For those remuneration committees who heeded shareholder advice and chose to modify grants downwards, in an effort to mitigate windfall gains, the question will still remain: did they reduce grants correctly?

Final Thoughts

Whilst earlier in the year we were advising our clients to sit tight and fully assess the situation before acting, the year-end now looms. Remuneration committees are going to have to make some tough calls but the message from shareholders is clear: “any pain should start at the top.”